DCF Conclusions on Google (GOOG)

GOOG DCF Conclusions Shared + Daily Journal for Today

Hi Folks,

What a day. I practice gratitude every day, but I am feeling especially grateful today.

A quick note on markets before getting into the Google DCF.

Today, the market saw an incredible bailout towards the close of the session, where a meaningful percentage of daily declines were recovered. My journaling of this session can be found here (on Instagram), and I am extremely grateful for this incredible recovery at the end.

We can see that markets became much more unfriendly in a hurry after Apple’s disappointing fundamental data from China.

As I’ve been doing over the past few weeks, I’ve been spending lots of time compiling the DCF Conclusion Study for all Mag7 stocks.

Readers were most likely very well prepared for weakness in Apple and Tesla, as those were the primary conclusions that our DCF Conclusion Study discussed.

For this reason, to help my readers, I’m making several DCF Conclusions on the Mag7 available to the public - where folks can read our warning on Apple and our lukewarm thinking on TSLA.

Here are the links:

Apple DCF Conclusion Study (Made available to help the Public)

Tesla DCF Conclusion Study (Made available to help the Public)

Today’s DCF Conclusions for Google, is also made public to help the Folks.

If my research is helping you, please consider helping our research efforts by supporting our work.

Google DCF Discussion

Google’s Ads business has encountered a lumpy period where certain quarters see its Youtube segment perform better whereas others see its Search business do well.

In a bid to compete with ChatGPT, Google’s AI called Gemini was released to the public to gain traction but so far has experienced a few blunders which have generated adverse press.

Google is one of the Mag7 stocks that is going through a corrective cycle.

We’ll discuss below at what levels the company may see better days ahead.

GOOG Fundamental Core Figures in 2024

Here are the conclusions that I’m drawing (No comparable to 2023 because I didn’t make a GOOG DCF in 2023)

Wall Street Consensus Revenue estimates that GOOG is poised to grow in the 10% top-line profile and then gradually slow down into a high-single digit compounder in its terminal years 2027-2028

Revenue Growth RATES estimates are slowing down into the terminal year because the Street expects maturity and saturation in the Ads business, where GOOG already has a leadership position.

EBITDA margin estimates are taking a big step up from today’s levels of low 30% into the mid 40% region. If this plays out the way the Street expects it to, GOOG has significant upside from here. However, as will be discussed below, I think mid 40% EBITDA margins is too ambitious.

We can see in the chart above that the Street expects Google to revisit its corporate highs in terms of profitability (EBITDA margins) in the coming years, up from 31.8% today to the mid 40% region by 2027-2028.

The Street’s estimates are due to a changing business mix which includes more EBITDA contribution from generative AI revenue sources as well as continued strict management of its cost structure.

I believe that Google does have margin expansion opportunity from here up to high 30% region, but reaching the mid 40% region is a path that I think will be more difficult than current estimates convey.

This is because to build out the firm’s generative AI capabilities, there will be significant Capex involved. And because ChatGPT is the current dominant Chat-Bot used by consumers, Google may have to allocate more marketing dollars to attract users to use Gemini.

As it stands, Gemini has not gained much traction with consumers and I don’t expect this to change without significant marketing expenses given ChatGPT is a very good option and Microsoft is also leveraging its Co-Pilot GPT bot.

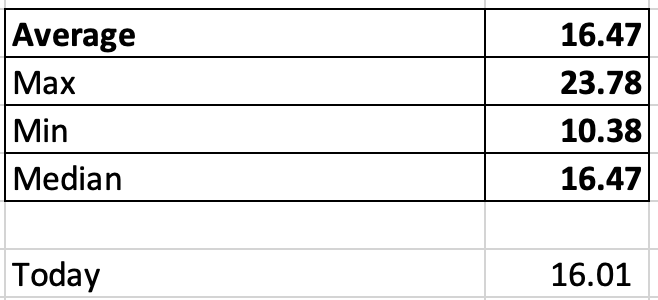

Historical Valuation Data for GOOG EV/EBITDA

Here is the historical range of EV/EBITDA multiple over a 10 year period.

Today it is 16X

Average is around 16.47X

Median is also around 16.47x

Google’s valuation multiple is trading in line with its historical average. For this reason, I do not see valuation as a concern when it comes to analyzing its equity value.

That being said, because GOOG is now facing a stronger and more formidable Meta in the Ads industry, in most of my DCF scenarios below, I will not be assigning any valuation multiple expansion.

DCF Model Outcomes/Scenario Analysis:

The most important inputs in my opinion are 1.) Top Line Growth (Sales) 2.) EBITDA Margins (profitability) and 3.) Valuation Multiple EV/EBITDA (what Investors Pay).

In all scenarios below, I will assume Wall Street Revenue estimates are accurate. The inputs that I change are EBITDA Margins and the EV/EBITDA Multiple. Changing revenue estimates do not move the needle by that much.

Similar to Meta, for GOOG - the Street has placed a large gap between the current margin profile compared to the estimated margin profile is quite large. The Bull Case will use the estimated Street margin profile. The base/bear cases will use today’s margin rates or a stress-tested version of it.

In all cases below, I will not give valuation multiple expansion out of conservatism.

Scenario 1 Assumptions:

Wall Street Revenue Estimates for 2027-2028 are accurate

Terminal Year EBITDA margins are 43% (Currently the Terminal Year Estimate)

Apply a 16X EV/EBITDA multiple (same as today)

195-200/share

Note: The Street is using an optimistic 43% terminal margin assumption whereas the corporate high in Google’s history is 39%. I don’t personally think it will be easy to achieve that degree of profitability for Google. This scenario is the most optimistic, and may take more than 1-2 years to play out.

Scenario 2 Assumptions:

Wall Street Revenue Estimates are accurate

Terminal year EBITDA Margins are 32% (Current Level-Today’s EBITDA margins)

Apply same 16X EV/EBITDA multiple (Same as today)

150-155/share

Scenario 3 Assumptions

Wall Street Revenue Estimates are accurate

Terminal Year EBITDA Margins are 30% (Last seen during Covid in 2020)

Apply 14X EV/EBITDA multiple (10% valuation haircut)

138-140/share

Scenario 4 Assumptions

Wall Street Revenue Estimates are accurate

Terminal Year EBITDA Margins are 28% (10% Margin Haircut from today)

Apply 14X EV/EBITDA multiple (10% Multiple Haircut from today)

120-125/share

Commentary:

Trading at the 130-135 range currently for GOOG, it appears the Buy Side is taking the glass half empty perspective as it gravitates under Scenario 3 (138-140) and towards Scenario 4 (120-125), which is a situation where we apply a 10% haircut to EBITDA margins and a 10% haircut to the historical valuation multiple.

My opinion is that if GOOG does reach Scenario 4, buying long-dated Calls with Strike 130 or buying it directly will most likely reward traders with a sufficiently long-enough timeframe.

I do not think Scenario 1 is likely to play out over the short-term. But I do think that Scenario 2 is feasible by year end if markets remain stable.

GOOG PlayBook:

Risk-Averse: Sell Puts into 120-125 as that region looks good to me for long-term holdings

Risk-Tolerant: Buy Long-Dated Calls if we enter 120-125 with Strike 130.

Reasonable target is the 150-155 area within a one year period. The outcome from Scenario 1 (190-200) may take 2-3 years to play out.

Conclusion: It doesn’t appear to me that Google is a Mag7 stock that is high-risk to the market. At the same time, it has fewer upside Scenarios than Meta, AMZN, MSFT, and NVDA.

If 120-125 is seen, that area should reward Investors.

As shared in previous DCF Conclusions, I view Apple and Tesla to greater risks to the broad advance.

You can read my reasoning on why I was most bearish on Apple out of the Mag 7 with links below.

-Larry

Multi-Timeframe Thinking:

Intraday: Will share 3/6 Thoughts in Pre-Market.

Intermediate-Term: As previously mentioned, I like PDD & ORCL at today’s prices for a multi-month Hold.

Long-Term: Waiting for some of the Mag7 stocks to gravitate towards my Bear Case Scenario, which will be when I begin scaling in.

Link to DCF Archive (Mag7): https://larrycheung.substack.com/t/dcf-modeling-fundamental-analysis

Note: These are my opinions based on my own research and my model may or may not aligned to the market’s thinking. I have to repeat this in all my notes as there is an element of the unknown in today’s strange macro environment.

Disclaimer: My investment community is not investment, financial, or trading advice, but for educational informational purposes only. I am happy to share my personal opinions which I provide as my personal journal. Trading of any kind of securities involves a lot of risk. No guarantee of any profit whatsoever is made. Investors may lose everything they have. Practice extreme caution. No profit is guaranteed whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this publication are NOT registered as securities broker-dealers or investment advisors either with the U.S. SEC, CFTC or with any other securities/regulatory authority. Make sure to consult with a registered investment advisor, broker-dealer, and/or financial advisor.