Public Commentary: Rates Will Enter Restrictive Territory And A Recession is All But Guaranteed in the U.S.

Public Commentary: Rates Will Enter Restrictive Territory And A Recession is All But Guaranteed in the U.S.

A large decoupling has occurred between U.S. and World Markets. Will this decoupling last forever?

Note: This is an email note to my public audience. Please take a moment to be on my email list below, and share this note with other like-minded folks.

This note is designed to be more informal in nature compared to my other investment research updates as it touches upon social commentary and personal development. It is written to the public.

Follow me on social media for more interesting commentary as well:

Public Community & Readers,

Today on Capitol Hill, Fed Chief Jerome said the following line to our elected Congressmen:

“Nothing about the data suggests to me that we’ve tightened too much.”

Just a month ago, Jerome also said that the “disinflation process has started.”

What we are now witnessing is the extreme dangers of a data-dependent Fed that is now obsessively looking at each month’s data points to influence their decisions. This is all happening at a time when U.S. and China relations are reaching boiling points.

This email is about my own personal commentary about the road ahead for many folks as the Fed decides to tighten monetary policy further.

Let’s start here - the Terminal Rate expectations is now 5.5%+.

In simple terms, this means that monetary policy is about to get tighter in the U.S. (literally as we speak). Mortgage rates will go higher, credit card APRs will go higher, and so will auto loan rates.

Market participants are expecting that the Fed Funds rates will now peak higher than previously thought, and if this trend continues, it’s hard to ignore the fact that even 6% terminal rates may be on the table.

Here’s how that becomes quite problematic from a macro standpoint:

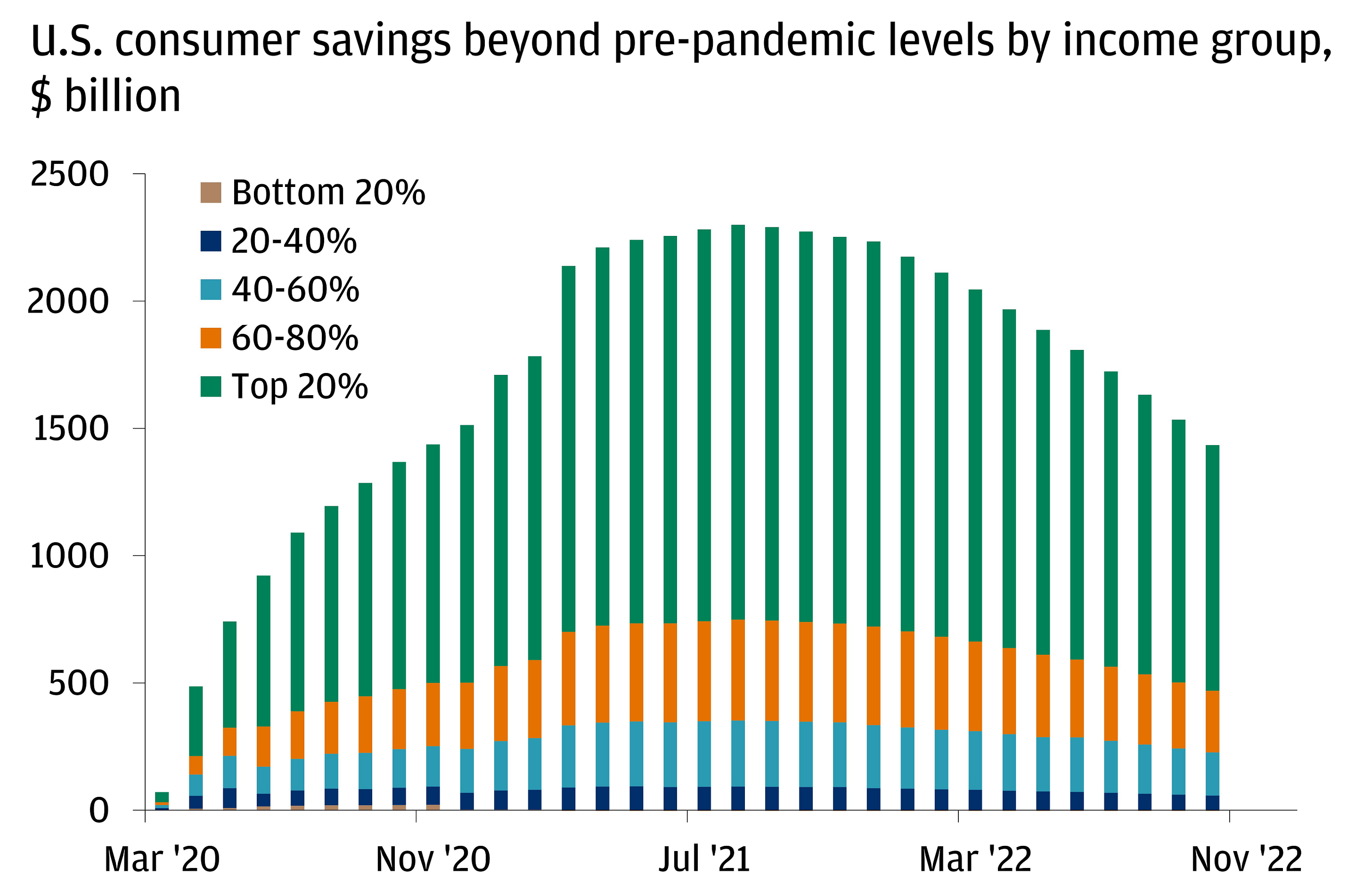

There’s now $986 billion in Credit Card debt in the U.S.

$1.6 trillion in auto loans outstanding

$11.6 trillion in mortgages outstanding

And $16.5 trillion in household debt overall

Debt is essentially at record highs, and savings is essentially at record lows.

And it’s not difficult to tell that this dynamic is going to continue - but how much longer can this trend last without something breaking in the system?

According to a new Bankrate report, it was revealed that “more than a third (36%) of U.S. adults owe more money in credit card debt than they have saved. This is a record high in its 12 years of polling Americans, and a significant jump from the last two years where that percentage was at 27% and 22% in 2021 and 2022, respectively.”

Given that credit card APRs are variable, we are entering an environment where a significant group of people will now be on the hook for larger and larger interest payments that compound over time.

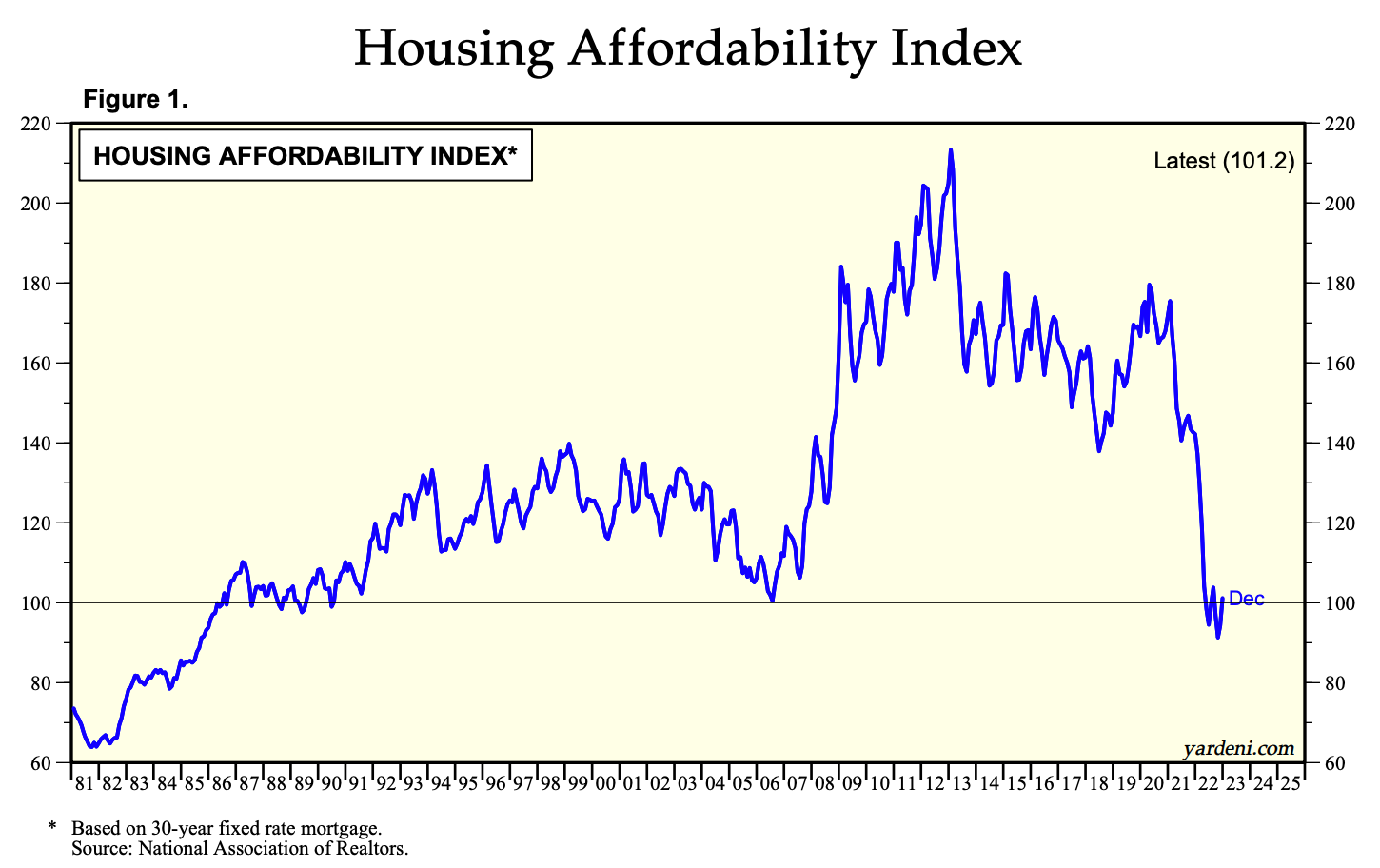

And if we look at data surrounding the Housing Affordability index (published by Ed Yardeni), we’ll see that housing hasn’t been this unaffordable since 2006 (briefly) and then back to the 1980s.

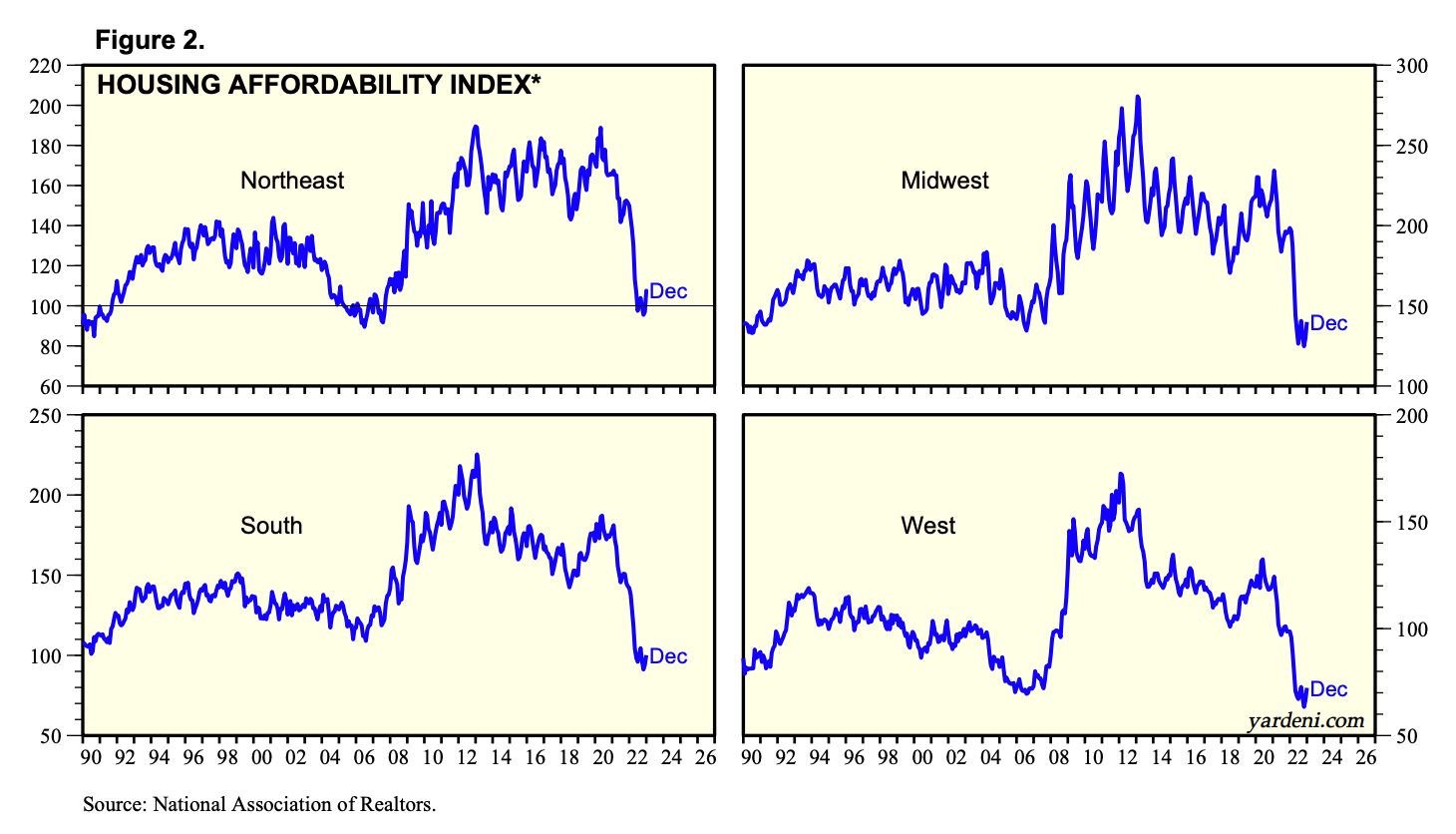

If we break down the geographies in the U.S., you’ll see that every other region besides the Northeast is essentially at all-time lows in terms of affordability.

Home ownership is important for most people living in the U.S. as it represents the typical American of climbing the “property ladder” (which is ironically a term originating from the U.K).

With interest rates as high as they are today and inflation remaining persistently high, making it onto the property ladder is becoming more and more difficult.

What we are witnessing is a gradual (but extremely obvious) phase-out of the middle class and a narrow tunnel that has been formed for a select group of people to get ahead in life.

I mean, after all: these high interest rates benefit people who have ginormous cash balances while hurting every day folks’ 401Ks that are invested in the markets for their future retirement.

This brings me to the next part of my note, which is advice that I’d like to share:

On home ownership and real estate: Now is most likely not the most optimal time to purchase a home especially if you work in an interest-rate sensitive industry

On stocks: The U.S. stock market has ephemeral pockets of value and tradable moments. But for pure buy & hold investors, this is an exceptionally challenging environment with valuations for many companies still unhinged from economic reality

On social/relationships: The best thing that you can do right now is to spend more time with loved ones and build a circle of friends who you can depend on. This will improve your mental health and strengthen your resolve when things become more challenging (which they will).

On personal development: 2023-2024 will be a pivotal period of time for people who build valuable skills to propel their career and net worth into the next bracket higher once “normalization” of interest rates occurs.

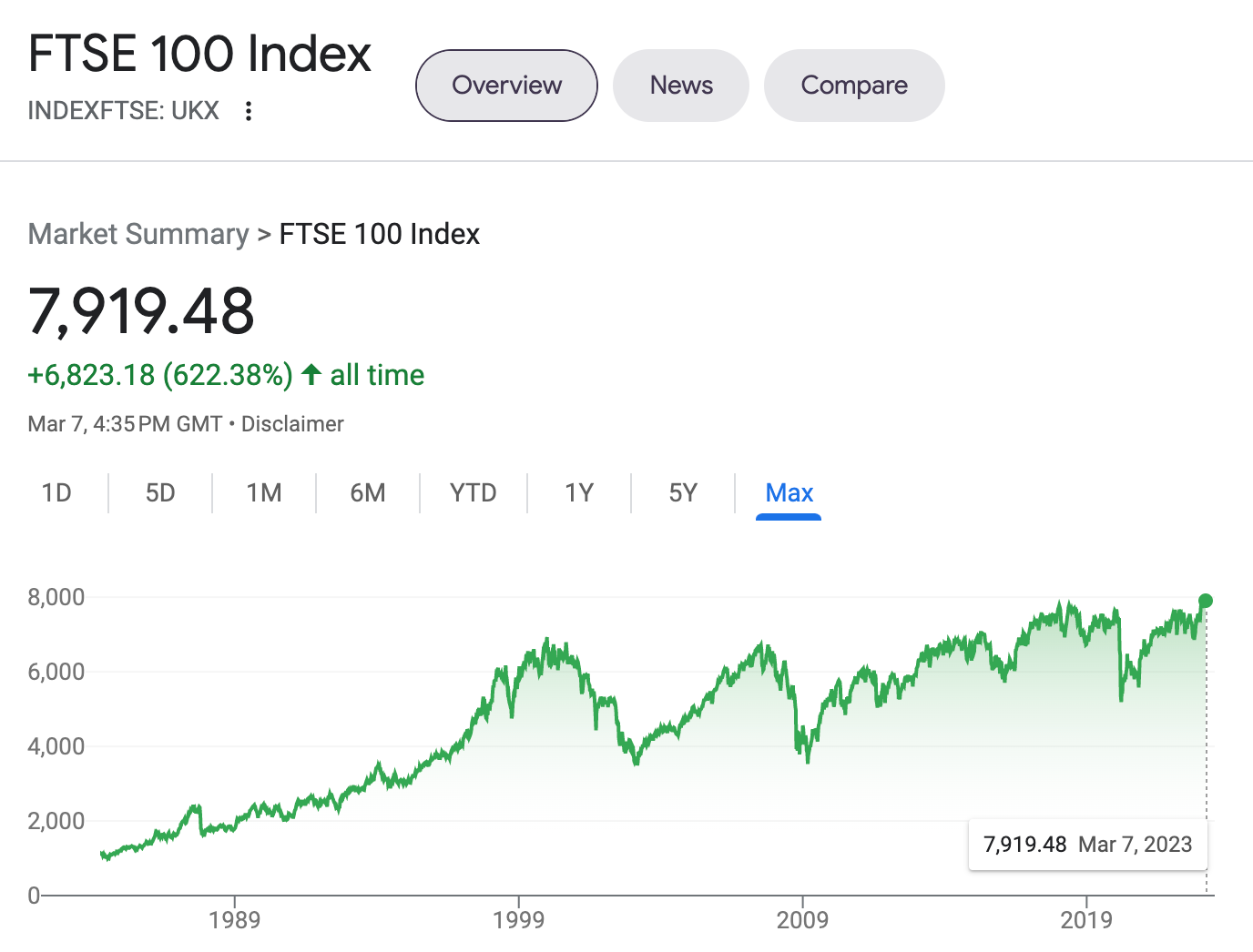

When I look at global markets outside of the U.S., I see several markets near all-time highs - despite all the global economic uncertainty we read on a daily basis.

Australia near all-time highs

London near all-time highs

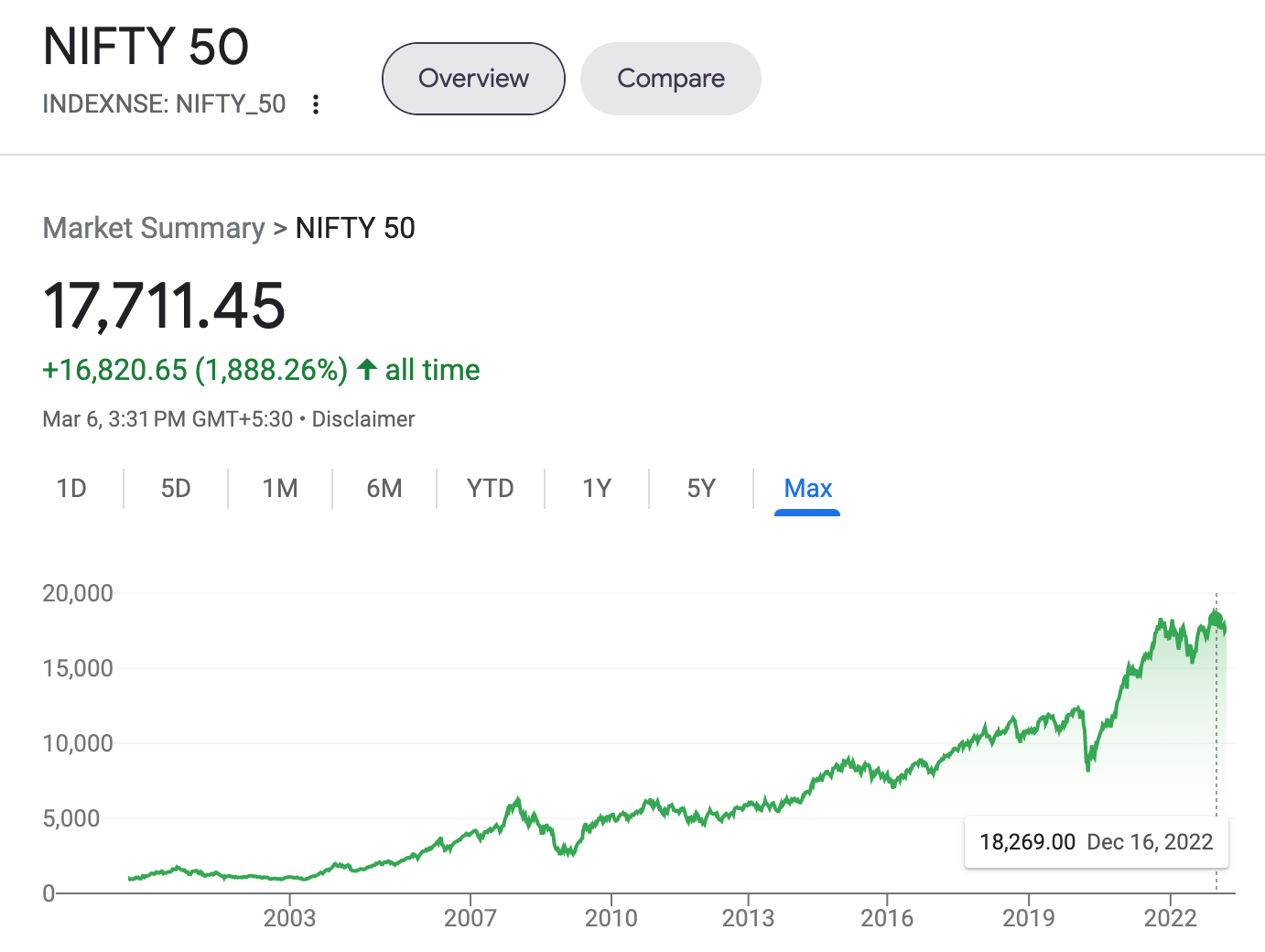

India near all-time highs

Canada near all-time highs

While my own personal specialty is currently in U.S. and China markets, this rather extreme decoupling between U.S. and global markets has gotten my attention.

One curious question that we might ask is: Will U.S. & China markets recover like their Global peers? Or will Global peers peak soon, and follow the downturn in the U.S. and China?

Going forward, I may allocate a very small, minority percentage of my research time to assess the global landscape and its opportunities via suitable global ETFs that may be appropriate at the right time for members inside my community.

U.S & China markets continue to be my bread & butter expertise, and I intend to further the edge in my core specialty as that is where my highest conviction opinions come into play.

In the meantime, I’m rooting for all of you, and will keep you updated on my socials across Instagram, Twitter, and Youtube.

This upcoming U.S. recession will be one of the greatest generational opportunities of our lifetime to move up the social ladder by at least 2-3 notches if you’ve been patiently preparing for this moment.

Do everything you can to get ahead in the coming 12-18 months - opportunity is coming!

~Larry

Social: