Micron (MU) DCF Conclusion Study

The King of Memory Likely Has Substantial LONG-TERM Upside. This is Not 0DTE.

Hi Everyone,

Today we’ll run through the DCF Conclusion study for Micron (MU), which is the 6th most important company within the SOXX ETF as of this post.

A reminder that this week is quarterly rebalancing, and we can see below that a number of weighting changes have happened to the SOXX ETF in the past few days.

AVGO moved up to 1st place in terms of weight

NVDA is 2nd. It was previously 1st.

Qualcomm went from 3rd to 5th

AMAT rose from 9th to 4th.

TSM moved from 5th to 9th

These rebalancing mechanisms - which usually take place at month-end and at quarter-end - do in fact play a role for traders (intraday/intermediate-term) as they reshuffle the focus list as to which stocks have most market-moving power.

For Micron, I was previously a bull earlier this year when it traded the 90ish region for a target to the low 100s. This upside expectation was too conservative in hindsight, but my model now is updated and will present key areas:

What is Micron’s fair value region today

What is the longer term upside potential

What are some areas that can be accumulated on Dips.

Semiconductors play a larger and larger role in the S&P 500 (and even the Nasdaq-100) than in previous cycles.

The logic is simple: by knowing the fair value of companies within the SOXX ETF (which are influential on ES and NQ), we position ourselves best as possible to understand where entry opportunities may be.

Every single new published/update DCF Conclusion Study on stocks that are important in the market increases our edge bit by bit.

Over time, this accumulated knowledge will compound into better market navigation.

Micron DCF Discussion/Context

Micron is one of the largest players in the memory space within Semiconductors, primarily focusing on DRAM and NAND memory chips. These chips, combined with Nvidia’s H200 GPU platform, serve as the infrastructure tools for tech companies to build out their AI products for the end market.

Being in the memory segment within semiconductors, Micron’s business model is more cyclical than say semicap equipment makers Lam Research and Applied Materials. This is because there are spot rates to memory chip pricing, which you can view here as an example.

I’ve included an example chart here to illustrate that DRAM memory chip pricing ebbs and flows with incoming supply & demand.

Because Micron’s business model is more cyclical than other peers within the SOXX ETF, its stock price can advance (or decline) at a velocity much faster than other SOXX stocks.

Micron’s stock is elevated, and a pullback would be preferred for longer-term entries.

For those who do not care about intermittent declines and only think about the final target, I think Micron is a $180-200 stock at the minimum given a 12-18 month timeframe.

In the shorter-term, pullbacks to 110-120 would be a healthy reload point. A deeper pullback to 100 is a STRONG buy.

With stocks that have large macro upside, almost all entries will eventually be profitable. The key then is acquiring them at lowest possible areas to maximize ROI.

Exhibit 1: DCF Core Figures from 2024

Here are the conclusions that I’m drawing:

We can see above that revenue growth estimates are going to see significant variance from year to year in the upcoming years. This is because as the memory goes through cyclical peaks and troughs, average selling prices (ASPs) for DRAM and NAND chips move up/down and this impacts the top line. Products that are in high-demand for the current AI development wave will allow 2024-2025 to be very robust years, which is why MU has risen almost 60%+ in 2024. Growth will moderate after 2025 as AI infrastructure spending matures.

For the purposes of EBITDA margin forecasting, I believe Micron is one of the more difficult companies within SOXX and NQ to forecast because its DRAM/NAND chips are constantly seeing pricing moves from constantly evolving perception of supply & demand. What I will do is be as conservative as possible with margin expectations.

We can see that there is an explosion of EBITDA growth from 2023 to the forecast in 2025 where EBITDA grows from $2.4B to $22.9B in a mere 3 years!

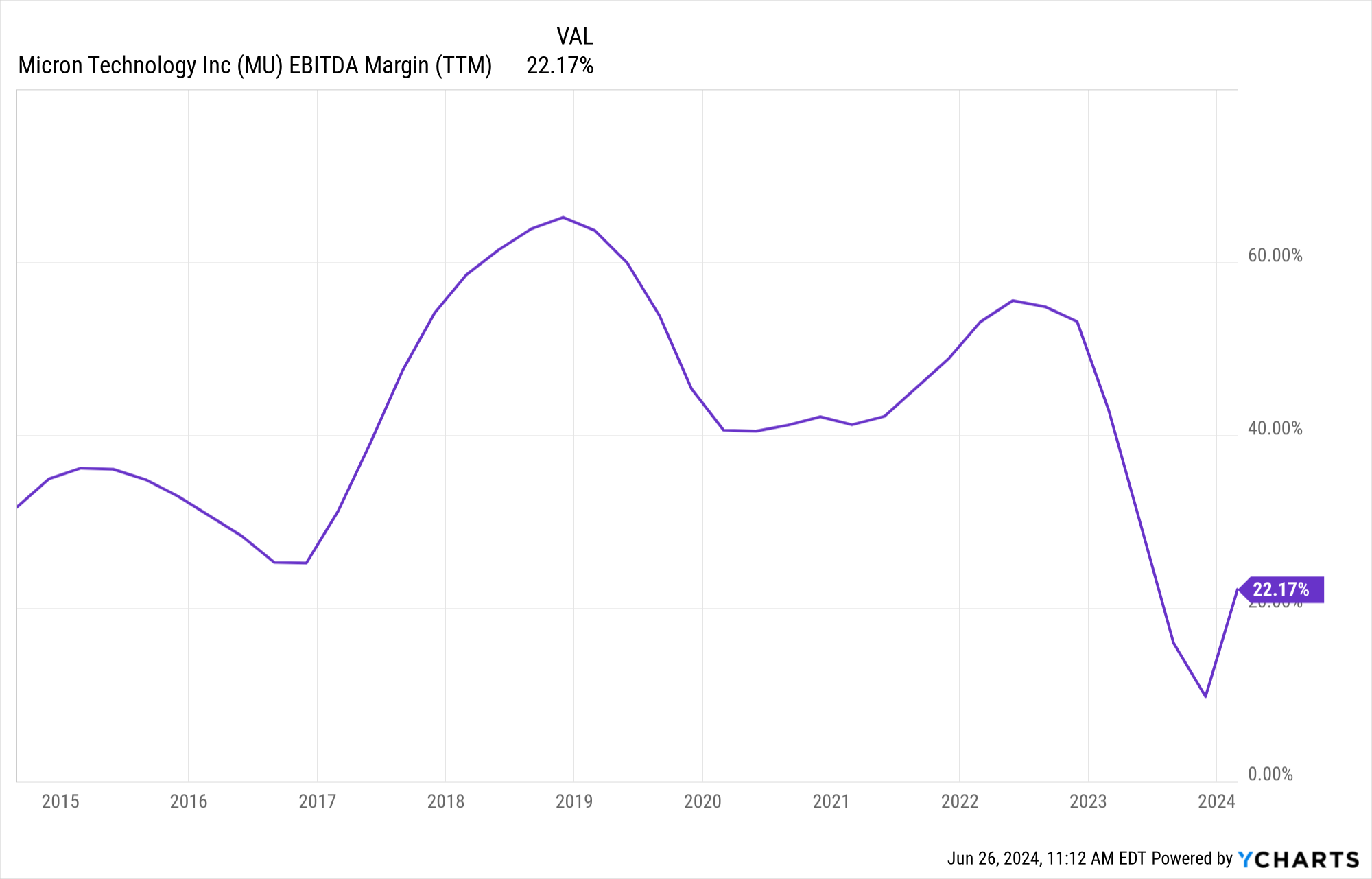

Margin Commentary (Margins are incredibly important to the DCF Model):

We can see below the memory industry (where Micron is a perfect proxy) has seen one of the sharpest downturns over the past 10 years during the 2022-2023 timeframe.

Micron’s stock was cut in half in 2022 (about a -50% return), but the Street’s forecast that margins and total EBITDA would lift in 2024 sparked a tremendous rebound in 2023 (stock was up 70% in 2023).

The bottom line is that Micron will follow its margin and EBITDA trajectory (as do most stocks). Because margin and EBITDA trajectory expectations change rapidly, its stock is very high beta compared to NQ’s FAAMG stocks.

Valuation

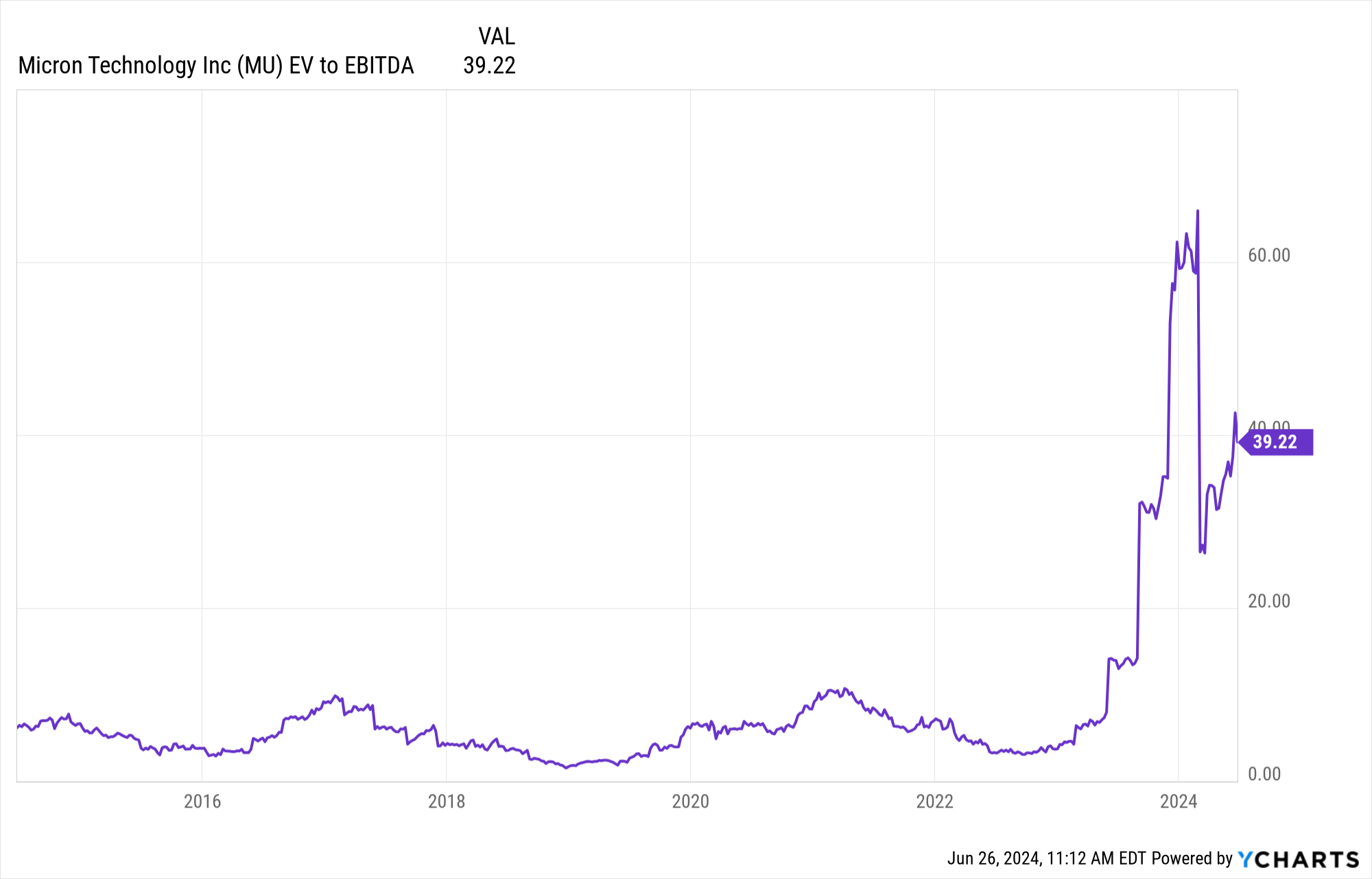

Rising expectations that Micron will be well positioned to serve the AI market with its leading position in memory has pushed its valuation into a new paradigm compared to the previous several years.

Previously, before the AI surge, Micron traded on average between 8x and 10X EV/EBITDA.

The 18-month valuation average in the AI-driven environment is closer 30X, for a good reason of course.

In other words, Micron has been re-rated higher due to its market-product positioning, and if the company can manage to diversify slightly from the boom-bust cycle of DRAM/NAND chips, I believe its valuation today is reasonable and that larger forward EBITDA estimates will lift the stock in the long-term.

DCF Model Outcomes/Scenario Analysis:

The most important inputs in my opinion are 1.) Top Line Growth (Sales) 2.) EBITDA Margins (profitability) and 3.) Valuation Multiple EV/EBITDA (what Investors Pay).

In all scenarios below, I will assume Wall Street Revenue estimates are accurate. The inputs that I change are EBITDA Margins and the EV/EBITDA Multiple. Changing revenue estimates do not move the needle by that much.

Scenario 1 Assumptions:

Wall Street Revenue Estimates are accurate

Terminal Year EBITDA margins are 42% (10-Year Average 2014-2024, below the Street terminal rate of 55%)

Apply a 20X EV/EBITDA multiple (BELOW the 39X EV/EBITDA Multiple today)

250-260/share

Note: This is a big long-term macro bull case for Micron. Looks ambitious because it’s almost 80% higher than today’s level. Obviously, this will take time to materialize. Can this happen? Based on my DCF, yes, but it will take a few years.

Scenario 2 Assumptions:

Wall Street Revenue Estimates are accurate

Terminal year EBITDA Margins are 30% (Below 10-Year average of 42%)

Apply same 15X EV/EBITDA multiple (FAR BELOW the 39X EV/EBITDA Multiple today)

185-190/share

Note: This is a realistic investment target. Obviously, the lower the entry point, the higher the ROI when 185-190 is achieved.

Scenario 3 Assumptions

Wall Street Revenue Estimates are accurate

Terminal Year EBITDA Margins are 30% (Below 10-Year Average of 42%)

Apply 8X EV/EBITDA multiple (10-Year Long-Term Average)

130-135/share

Note: I’d say this is fair value for MU. Anything significantly below this area will begin to catch my interest.

Scenario 4 Assumptions (Mega Bear Case)

Wall Street Revenue Estimates are accurate

Terminal Year EBITDA Margins are 20% (Below 10-Year Average of 42%)

Apply 5X EV/EBITDA multiple (Tremendous valuation haircut on multiple)

98-105/share

Note: That level if seen, or even the 110-120 area, is likely going to be good for long term accumulation.

Commentary:

Similar to the Broadcom DCF Conclusion where I observed serious upside potential, an equally similar story could be in play here for Micron from an investment standpoint (longer timeframe is required).

Obviously, the stock has run up significantly in 2024 and chasing here in a completely new entry makes little sense ahead of earnings (even if does go higher).

The strategy here then is that I think if Micron sees Scenario 4 (~100 or something close to it) at some point this year if we finally see a semiconductor correction, that area is a prime area for accumulation.

If there is no meaningful dip in semiconductors, interested Investors in Micron may have to bite their tongue and see if Scenario 3 is offered and then Hold for Scenario 1 & 2 in the coming 12-18 months.

Just like the Broadcom situation, Micron is a stock that has clear long term upside.

The only question then is what is the entry, because that will determine the ROI.

Within 18 months, any entry in Micron (in my opinion) below 140 will be profitable because it’ll be trading new highs anyway.

-Larry

Important Links (Organized DCF Conclusion Studies By Indices)

Semiconductor SOXX ETF Top Stocks DCF Conclusion Studies (Newly Added - will add the other SOXX names in here shortly): https://larrycheung.substack.com/t/soxx-etf-top-10-dcfs

DOW Top Stocks DCF Conclusion Studies:

https://larrycheung.substack.com/t/dow-etf-top-10-dcfs

QQQ ETF Top Stocks DCF Conclusion Studies: https://larrycheung.substack.com/t/qqq-etf-top-10-dcfs

SPY ETF Top Stocks DCF Conclusion Studies: https://larrycheung.substack.com/t/spy-etf-top-10-dcfs

Conclusion Table on Dow and QQQ ETF Stocks

Link to DCF Full Archive: https://larrycheung.substack.com/t/dcf-modeling-fundamental-analysis

Link to Educational Guides: https://larrycheung.substack.com/t/educational-guides

Q&A: Why I focus on NQ as a primary market.

My focus: I now focus about 95% of my attention on price action when it comes to the indices. I would strongly encourage spending lots of “screen time” for folks who want to navigate the market.

Note: I publish Monday-Thursday. These are my opinions based on my own research and my model may or may not aligned to the market’s thinking. I have to repeat this in all my notes as there is an element of the unknown in today’s strange macro environment.

Disclaimer: My investment community is not investment, financial, or trading advice, but for educational informational purposes only. I am happy to share my personal opinions which I provide as my personal journal. Trading of any kind of securities involves a lot of risk. No guarantee of any profit whatsoever is made. Investors may lose everything they have. Practice extreme caution. No profit is guaranteed whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this publication are NOT registered as securities broker-dealers or investment advisors either with the U.S. SEC, CFTC or with any other securities/regulatory authority. Make sure to consult with a registered investment advisor, broker-dealer, and/or financial advisor.