Feb Investment Strategy (Mid-Month Part 2): The Market's Near-Term Momentum is based on Hopes and Dreams. Will they come true?

Preview Included: Premium Report for Members - Part 2 Feb Mid-Month Report

Note to Readers: This note is Part 2 of my mid-month strategy note for February.

A note to some of our newer members: just a reminder that my strategy is very focused on Intermediate-Term investing and guidance on markets directionally looking out several weeks and months. I’ve had a couple folks (inside my Community) ask me if I offer a signal service for instant day trading alerts and misunderstand the nature of my Community.

Please understand that while I do share my opinions and viewpoints, the guidance provided is intended to be longer-term in nature and is not an intraday alerts service.

Members,

This note will serve as Part 2 to my February Mid-Month Report.

Before we begin the note, I want to talk about a few updates I’ve made to the Research Dashboard - changes that I believe you’ll find helpful.

The Research Dashboard now includes stocks from the following context:

The top 25 SPX Names by Weight (Controls ~40% of the index)

The top 10 DIA Names by Weight (Controls ~50% of the index)

The top 25 QQQ Names by Weight (Controls ~50% of the index)

The top 10 names in the KWEB ETF (Controls ~40% of the ETF)

*Will add top 10 names in the SOXX ETF by next update (Controls 50% of the ETF*

Together, these ~50 names essentially influence nearly half of the market’s directional movement. Understand the fundamental, macro, and technical direction of these individual companies, and you will have an objective bottom-up assessment of where the indices (S&P, Nasdaq, Dow, KWEB ETF) are headed.

The Research Dashboard (at the bottom of this email) contains the following information to help members understand market structure from a bottom-up perspective and dramatically cut down on research time on companies to help them assess risk/reward at a broad market level.

RSI Levels

Short-Term, Intermediate-Term, and Long-Term Moving Averages

1-month, 3-month, 1-year total returns

Forward P/Es of every company, relative to its 3Y and 5Y medians.

Sharpe Ratios and Standard Deviation Metrics to assess how large the monthly swings are in the names

Any applicable dividend yields

I intend to share my key opinions and bias on these names (and more) periodically and selectively in this Newsletter here.

I may also discuss names outside of the Research Dashboard as I’m now constantly studying new stocks and opportunities to add to my watchlist to find opportunities in this landscape.

A few highlights since our previous strategy note where I shared a view on names with a directional bias:

One of our Top Ideas in January was the UUP Dollar ETF (discussed at 27.5), which has since performed exceptionally well for a low volatility currency ETF, all things considered. Now 28 or so. This is about a 2% return while the SPX returned 3-4% over the timeframe. However, UUP had almost zero drawdown since January while SPX’s volatility makes even the strongest traders question their beliefs. Remember the importance and value of a high sharpe ratio (balance between returns and standard deviation of returns).

CF Industries (discussed at 84) also made a trip from 84 to 91 before its recent retracement back to 85.

ZIM (discussed at 19) made a trip from 19 to 23, before its recent retracement back to 21 or so.

BABA (discussed at 120 with a bearish view) made a trip from 120 back to 102. I still like China long-term and still Hold (as you will see in this note below), but as a public strategist, my goal is to help you understand risk/reward on the upside/downside and not marry any particular stock. I am here to help you make money/manage risk (or lose less in very difficult environments), and I’m not going to talk up a stock just because it’s a house favorite.

As a reminder, just like any analyst/strategist, I believe that I do have an edge when it comes to directional opinions on names that I have studied closely.

However, how long a stock stays at a certain level, I cannot be certain and is impossible to determine.

Stocks prices are incredibly ephemeral and need to be treated as such.

With that said, February’s mid-month Part 2 of the Newsletter has a couple questions that I wish to answer for the good folks here, which I’m sure is top of mind:

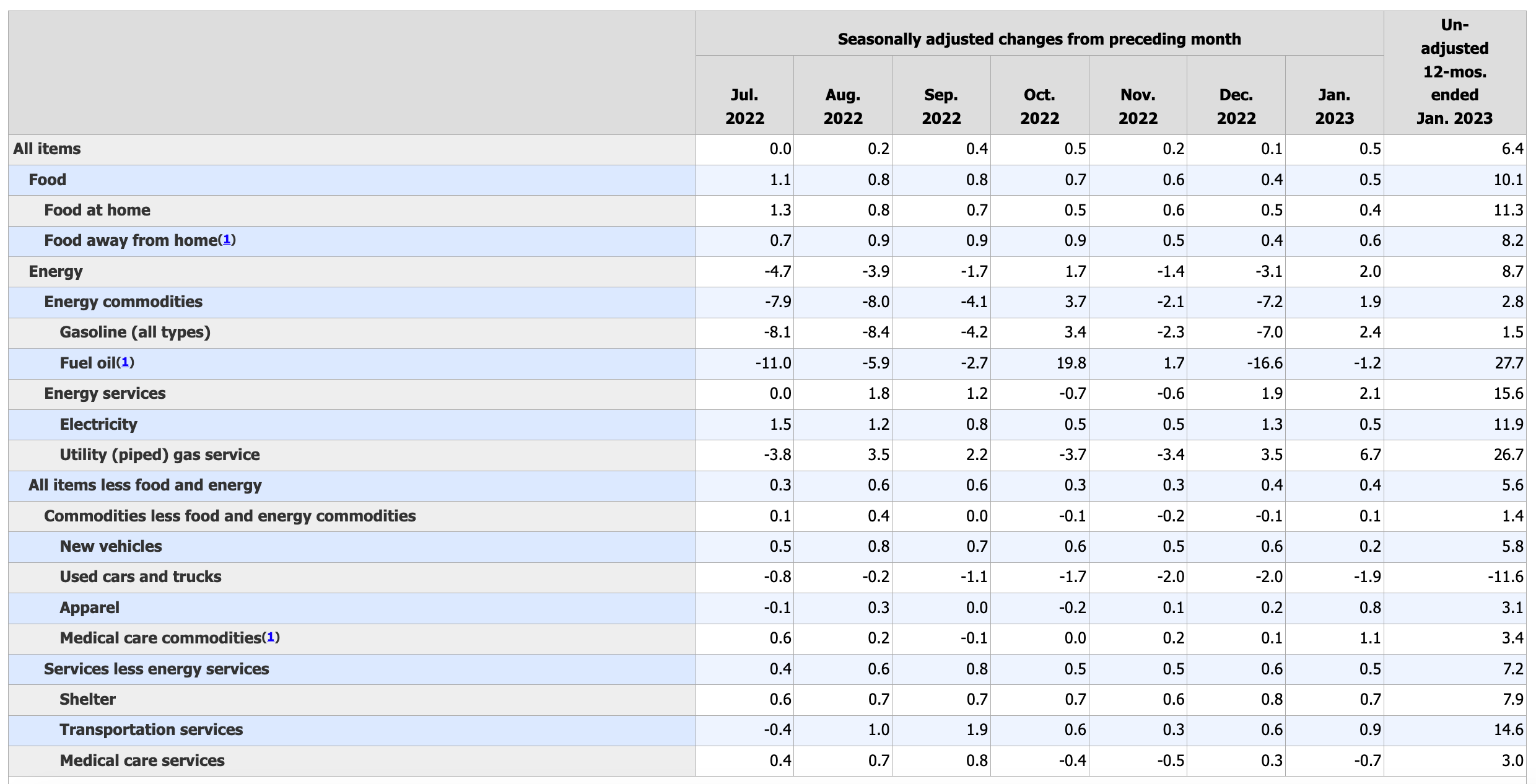

A very quick recap of Inflation from January 2023 and the implications behind a 6.4% reading.

Why are the markets rallying even though Inflation is remaining stubbornly high?

What is my outlook for the China theme over the coming months?

Where is there still opportunity in this very expensive market?

At the end of this note, I’ll provide some names/themes where I see a retracement taking place at some point in the coming 3-6 months (to help members be psychologically prepared).

Yes, that’s right - in this note, I’m listing potential Downside targets on a number of companies that I’m watching.

The market’s near-term momentum is exceptionally solid. But momentum is based on the assumption that fundamentals are sound.

What if the fundamentals…are not so sound?

Make sure to read my previous commentary from December to January to understand my views up until now.

Inflation CPI: With January’s figure at 6.4%, we begin the path of a more challenging (and more drawn out) fight towards lower CPI figures.

First, I want to remind the good folks here that the Fed is really focused on a figure known as “Services Ex-Housing.” In Jerome’s previous couple press conferences, he’s emphasized heavily on this part of the inflation data. Some economists refer to this as “Super Core Inflation” because it strips out the delay of the Housing component’s lag in the data (see trends below from 2022 on Super Core Inflation).

In January’s 2023 CPI Figure, Super Core Inflation continued to see price increases, and weakens expectations on dramatic disinflation that the Fed wants to see in this category.

This may partially explain why the 2Y Yield rose to 4.6%+ after the data release as traders know this specific component of CPI is closely watched by the Fed.

On top of a stubborn Super Core Inflation reading, the past several months of CPI has been revised higher.

Yet, the market continues to demonstrate relatively strong resilience. Stocks that were battered in 2022 have received the most attention in 2023.

A potential explanation behind this market’s behavior is that market participants seem to believe the following things:

That near year 2024 S&P 500 EPS will be better than feared

That Inflation is coming down to the Fed’s 2% Target

That a Soft Landing (slower growth without a spike in unemployment) is increasingly likely

Also: That Chat GPT (AI) will ignite a cycle of innovation, with its potential now spreading optimism into the Semiconductor industry and Microsoft - two of the biggest themes and components in the entire tech sector.

To be clear, I think all 4 points above are going to end up being a mirage. This, however, could take at least several months to play its course.

Price action has the ability to persuade a significant number of market participants, and even force institutional investors to chase the rally due to performance management.

To support the Soft Landing narrative, Goldman Sachs’s CEO David Solomon has recently come out to say that the odds of a soft landing has increased after the CPI report. Yet, Goldman just made one of the biggest headcount restructuring decisions in its corporate history. In fact, laid off Goldman Analysts didn’t even receive their traditional year-end bonuses if they were cut. A soft landing maybe for Managing Directors, but not for the thousands of Analysts employed by GS.

Media headlines from the Bulge Bracket banks have the ability to convince retail investors that the tides are changing. There is a growing camp of folks who are increasingly convinced that a soft landing will materialize.

Whether you agree with this statement or not from an economic level depends on who you are individually and what your background/occupation is.

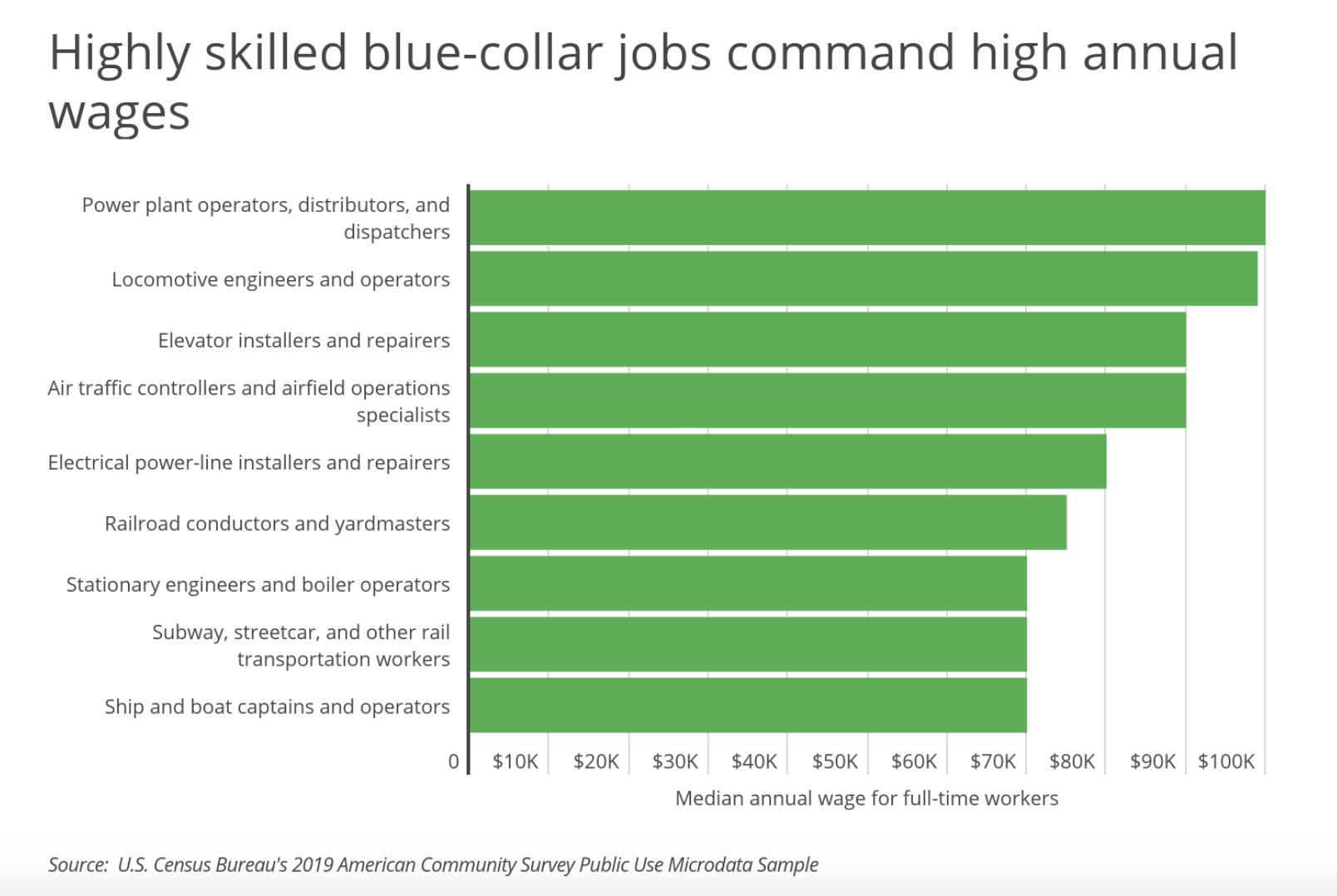

The U.S. labor market is going through a subtle transition at the moment - where Blue Collar workers now see their prospects being strengthened whereas White Collar workers have less leverage than before.

As time progresses, we’re going to see a cohort of White Collar workers get displaced by the current labor market reshuffling/transition that is happening as we speak.

For White Collar workers (as I’m sure you will agree), we are already in a deep recession, and the outlook has become more challenged than before.

For Blue-Collar folks where their hands-on services are more needed than ever before, they are now also busier than ever and have little fear that AI will someday come after their occupation.

It is this very dynamic that I believe partially explains the underlying resilience in the U.S. economy given the significance of Blue Collar workers’ contribution to aggregate consumption.

A few conclusions I wish to make now that I’ve contextually explained this:

Once we see a Blue-Collar recession, the next leg of the Bear Market will be immensely disturbing. As of now, Blue-Collar workers are holding up exceptionally well, and there are very few signs that this will let up soon.

Upon deeper inspection, the historically low unemployment rate in the U.S. is a signal that the Blue Collar workforce is alive and well. The layoffs in White Collar workers do not move the needle significantly in the unemployment rate. White Collar layoffs have an outsized impact on consumer spending, but it does not show up much in the macro data in the Unemployment rate, given that most of the layoffs have so far been concentrated in tech and interest-rate sensitive areas.

Essentially, Wall Street’s optimism on the S&P 500’s EPS figures for key consumer names hinges on their belief that Blue-Collar workers will continue to stay strong in this environment. The Street knows that White-Collar workers are experiencing a setback, but they expect that impact to not be broad-based on the U.S. economy.

With this being said, more important than the inflation figures, I logically believe we must now shift our focus to the following questions:

When does the consumption strength for Blue-Collar workers end?

How stressed is the consumer demographic for Blue-Collar workers?

What are the signals of big employers of Blue-Collar workers

Here is a list of the 20 largest Blue-Collar occupations for further reading.

As a reference point to understand the consumption strength of Blue Collar folks, many of the Blue Collar jobs on the list below typically pay between 60-80K USD, or more.

These jobs may not pay as much as tech and finance, but have much stronger job security than say an Investment Banker on Wall St.

And many studies from consumer psychology have proven that job security is a prime reason for consumer spending to remain stable.

It is my belief that once we see a softening in this part of the workforce (which I believe we will see later this year or in early 2024), the market will have a much more difficult time believing in a Soft Landing.

As you can see from the occupations above, many of them are not heavily interest-rate sensitive like occupations in housing, tech, or finance.

However, the companies that employ these workers is dependent on a healthy U.S-China relationship as increased import/export costs and inflation in raw goods will erode the profitability of these firms. These firms are also sensitive to a “wage spiral” due to inflation and labor unions organizing, which is the greatest fear at the Fed.

China’s economic reopening since Fall 2022 in my opinion has played a very positive near-term contribution to U.S. markets as it increases the probability that U.S. firms that hire Blue-Collar folks will see more stable supply chain relationships (and therefore stability in input prices) going forward. With these operating margin forecasts more stable, companies/industries in the chart above are likely to not engage in the scale of layoffs as interest-rate sensitive sectors like housing or tech.

However, if Inflation picks back up again and the tail risk is realized, these firms will engage in larger layoffs to shut off the expectation that wage growth will happen across its entire cost structure.

In my mind, layoffs are a powerful corporate mechanism not only to control the cost structure but to strongly signal to a firm’s employees to limit their expectations for salary increases and large inflation-linked salary bumps.

Over a multi-month period, widespread layoffs can single-handedly move down the “inflation expectations” charts that we see on Bloomberg or TradingView.

A Side Note on Fed Vice Chair Lael Brianard:

The Fed’s Vice Chair Lael Brainard will be appointed Biden’s top Economic Adviser. Given her reputation for being a Dove at the Fed, there is a discussion surrounding whether her leaving the Vice Chair post will make the Fed’s decision making committee more hawkish.

That could be the case, but that will not have an immediate impact on markets.

I personally think market participants should be focused on deteriorating corporate fundamentals, which are set to continue.

This was a side note. Back to the core research.

On China

Let’s talk about China for a moment very briefly.

In terms of markets, I had previously discussed my near-term view that BABA (China’s top consumption proxy) at 120/shr back in January was a very fragile price point. By late January, I shared my thinking with members that revisiting BABA 100 was becoming increasing likely based on my observations of the Chinese internet sector.

That has since happened, with BABA reaching 102 or so this week.

I do continue to believe that BABA and the China internet sector are in a multi-year recovery stage. For near-term traders, I think that 90-100 represent a good region for a 1st tranche re-entry to eventually retarget 110 or better.

As mentioned many times, I think China is a multi-year story, and KWEB/BABA’s recent retracement does nothing to change this view.

As a public strategist, I have to provide a near-term and long-term view so that Community members from different experiences/backgrounds will find my research applicable for them.

Looking out beyond markets, I want to discuss some fundamental considerations. Because there are quite a lot of news developments that I follow, I will use bullet points to express my views to be concise.

On China’s Domestic Affairs:

In a speech made in December 2022 in the Central Work Conference, General Secretary Xi Jinping discussed further support of private industries. Analysts continue to revisit his commentary to understand how policy is aligned in the business environment.

As a result, sentiment surrounding the business environment is becoming more friendly to private enterprises, but there is still lingering skepticism among the entrepreneur class in China that was burned by regulation back in 2021-2022.

On the Middle East/Saudi Arabia:

China and Saudi Arabia are forging closer ties, which will eventually allow the Chinese Yuan to gain more global prominence as commodity and oil transactions are partially priced in Yuan in the future.

On Geopolitics

The U.S. and China balloon saga is a development to be followed closely. In the near-term, the market risk premium on the China internet sector is raised to account for potential U.S. actions against any companies that is perceived to be a security risk.

I will be following developments surrounding Antony Blinken’s delayed/proposed trip to China.

On China’s Monetary Policy:

The PBOC is injecting more liquidity into China’s banking system to meet an increased uptick in loan demand

The PBOC’s contribution to global markets liquidity has been significant and is a core global markets have stayed supported

China’s correlation with U.S. Markets - will China stocks follow U.S. stocks into a recession?

Most Chinese firms within the KWEB ETF (like Alibaba, Tencent, Trip.com, etc) generate most of their revenue from China. So fundamentally, the stocks within KWEB follow the business outlook in Mainland China

Investors may notice that China stocks tend to track the QQQ, but that’s because these stocks are simply located in the QQQ index. As a result, when QQQ is moving higher or lower, these shares are also being indirectly bought or sold.

In the near-term during risk-on and risk-off episodes in the market, the correlation is high between U.S. and China equities. However, over a 3-5 year period, the correlation between KWEB ETF components and the S&P 500 or the Nasdaq is low, meaning that China is a long-term diversifier to a portfolio.

My net/net conclusion on China is that we are approaching areas where I will be interested again soon. However, I’m neutral on the sector at the moment and need to wait for further data.

I had high-confidence that China was attractive post 20th Party Congress when BABA traded 60 and high confidence that China’s 2023 run for BABA went too far as it approached 120-130. Both opinions turned out to be very correct.

At the present though, I continue to like China long-term but do not have a strong near-term view on the general sector.

My long-term constructive stance continues to remain unchanged in the face of near-term softness. The catalysts that drove China higher in December/January continue to be in place in February.

The only change since then has been higher equity prices.

On names/themes of interest based on economic environments

To wrap up this mid-month note, I want to take a moment to share with you some personal watchlist levels that I’m watching now.

On a macro level, my upside:downside ratio for the S&P 500 is still at 200:600 if we assume a 4200 level.

In other words, in the coming 6-9 months, I think we tap out at 4400 for a max upside target and could revisit 3600 if a negative feedback loop re-enters market psychology. This is a multi-month view, and not something that will take place this week.

If there is a large overshoot north of 4400 without a fundamental change in corporate earnings, I may start to discuss/provide education on short-selling in our Community as I personally believe those levels are strongly unwarranted if Fed Funds Rates range between 5% and 6%.

I want to provide a bit more context for other ideas that I’m also following.

My Base Case: Hard Landing, Weak EPS Outlook, and Tapped Out Consumer as a 2023-2024 Long-Term Theme

Continuing from my previous note I believe UUP ETF will reach 29/share within 6-months

Walmart, if accumulated between 130-135, is likely profitable as a holding with a 6-9 month horizon

Dollar Tree, if accumulated between 136-141, is likely profitable as a holding with a 6-9 month horizon

JNJ, if accumulated at 150-155 is likely a profitable as a holding with a 6-9 month horizon

GLD (Gold ETF), if accumulated at 155-160, is likely a profitable holding within a 6-9 month horizon.

Names that if approaching/nearing the following zones, I am personally interested in further research for long-term accumulation:

JD.Com (China Internet) at 45-50. I personally think JD is more attractive than BABA at time of this writing from a risk/reward perspective, looking out 3 months.

XOM (U.S. Energy) at 98-103

LMT (U.S. Defense) at 440

AMD (U.S. Semiconductors) at 65-70

BEKE (China Real Estate) at 16-17

BABA at 85-90

GOOG at 88-92

More names on my list, but will mention contextually at a later point to avoid this list being too long.

Possible 2023 Upside Potential Ranges In A Soft Landing Scenario (20% probability, in my view):

ARKK Names / Speculative Tech has about 25-35% upside from here

FAAMG has about 10-15% upside from here

China has about 15-25% upside from here

Semiconductors have about 10-20% upside from here

Consumer Discretionary has about 20-30% upside from here

Say the Soft Landing doesn’t play out, which I don’t personally think it will, then:

All the themes that I mentioned above has about 22-35% downside. China’s downside is most likely 15-20% rather than 30%+

Names/Themes that look have a potential setup for a retracement/further dip at some point in coming 3-6 months:

MGM Resorts currently at 44, could retarget/gravitate towards ~39.

NVDA currently at 227, could retarget/gravitate towards ~190

TSLA currently at 215, could retarget/gravitate towards ~185

SHOP currently at 48 (even after post-earnings selloff), could retarget/gravitate towards ~43 or lower

MU currently at 62, could retarget/gravitate towards ~55

Meta currently at 180, could retarget/gravitate towards ~150

BABA currently at 102, could retarget/gravitate towards ~90

MSFT currently at 270, could retarget/gravitate towards 245

TLT currently at 103, could retarget/gravitate towards 90-95 (a Strong Buy and a Gift to investors who know what they’re doing - in my view - at that level)

Yes, these names can all go up another 10% from today’s levels.

But I believe that it won’t take much for these retracement levels to be met.

At the index level, over the coming 3-6 months, I do believe that 290 or under could be retargeted on the QQQ ETF. As for SPY, I see 390 or lower in this timeline. For the SOXX ETF, I see 385 or lower.

I believe these levels will be eventually revisited and believe the probability of these retracement magnitude (or more) is about 60% (about the same confidence level that I had for BABA to retrace from 120 to 100 back in late Jan).

It’s not a super high-conviction opinion, but I think as long as the 2Y Yield or Dollar remain at today’s levels (or go higher), this will make a pullback more likely than not.

In other words, even if markets DO go higher in the near-term, I believe these retracement levels could still eventually be reached.

I am not convinced that we go straight up from here if the 2Y stays at 4.6% or DXY stays at 103 or higher. Even if we end the year higher from today’s level, I personally expect a retest of the levels mentioned above if 2Y is at 4.6%+ and DXY is at 103 or higher..

This may take quite some time, but I would be very surprised if we didn’t see a SPY 390 level - or lower - again (and its implications) at some point in 2023 given the fundamental/macro backdrop.

The reason I share these downside levels is so that our members have psychological preparation. Having psychological preparation is one of the greatest assets to stay strong during returning moments of volatility.

For this reason, even if there is further upside in markets, I’m going to be patient and wait for certain levels to come back to me and I’ll reassess the environment then.

The characteristics that explain this rally include strong liquidity, investor optimism, investor positioning, and a perception of strong disinflation.

I do not believe these characteristics will overweigh an increasingly weak fundamental backdrop and a U.S. consumer that is heavily dependent on credit (that could be maxed out later in 2023). The U.S consumer’s consumption strength is being fueled by credit card spending, as can be seen in the relative strength of V (Visa) and MA (Mastercard).

As we all know, Credit Cards have limits. They also have APRs of 25% (and are set to go higher later this year).

In the very, very near-term, the market’s momentum is unquestionably strong.

But that’s the problem: the only catalyst that I personally see that supports markets at the moment is momentum driven by liquidity and people/fund managers buying simply because the market is going higher.

That’s it for now - more strategy & research in upcoming posts.

Stay Safe,

Larry

Resources:

I can't seem to get the dropbox to work, it keeps on saying I need to signin to google, which I do. But it still doesn't load.