DCF Conclusion Study on United Health (UNH)

The most important company within the Dow Jones Industrial Average

Hey Everyone,

I hope everyone had a great Memorial Long Weekend. The Research/Data portion of today’s Premium Note will be released to all to celebrate the tremendous May that we are all having. The DCF Conclusions and its implications on trading the blue chip Dow Jones Index will be shared with Members.

We will discuss United Health (UNH), which is the most important price-weighted stock within the Dow Jones index (see image below).

While NQ (Nasdaq-100) is my primary market, I am actively studying Dow companies so that I can add the Dow to my trading skillset when technology eventually finds a soft patch (it will).

In the coming weeks, I will be looking to see if there is a “Sector Rotation” event where hot themes such as Semiconductors selloff violently but Dow Jones names are bid up. Trading sessions such as those make studying the Dow worthwhile as a defensive mechanism when primary sectors like technology experience weakness.

Because the Dow is a price-weighted index, this means the highest-priced stocks in the index have the most sway in where this index goes.

This means our Analysis on the Dow starts with UNH, the Dow’s highest priced stock.

United Health DCF Discussion/Context

Dow names have been a more challenging investment concept in 2024 as these companies tend to “feel” the impact of economic softness much more than NQ (Nasdaq-100) and ES (S&P 500).

If we get technical about the nature of the indices, NQ (and even ES) are essentially technology indices, which now mainly do business B2B, so their strength this year can bypass the weakness of the consumer (for now).

From a company specific standpoint, UNH has seen a more challenging backdrop due to the Centers of Medicare and Medicaid announcing a 2024 payment increase that disappointed investors looking for a bigger increase.

Investment Bank Mizuho estimated that the final effective rate for payments to Medicare Advantage in 2025 to be a decline of -.16% whereas the Street was looking for a 1% increase.

Exhibit 1: DCF Core Figures from 2024

Here are the conclusions that I’m drawing:

The Street is expecting UNH to turn from a double digit compounder into a mid-single digit growth story in the coming years.

The Street believes that UNH can grow EBITDA about 7-8% per year in the foreseeable future.

Analysts expect that EBITDA margins are likely to stay stable in the coming 3-5 years, with limited room for margin expansion

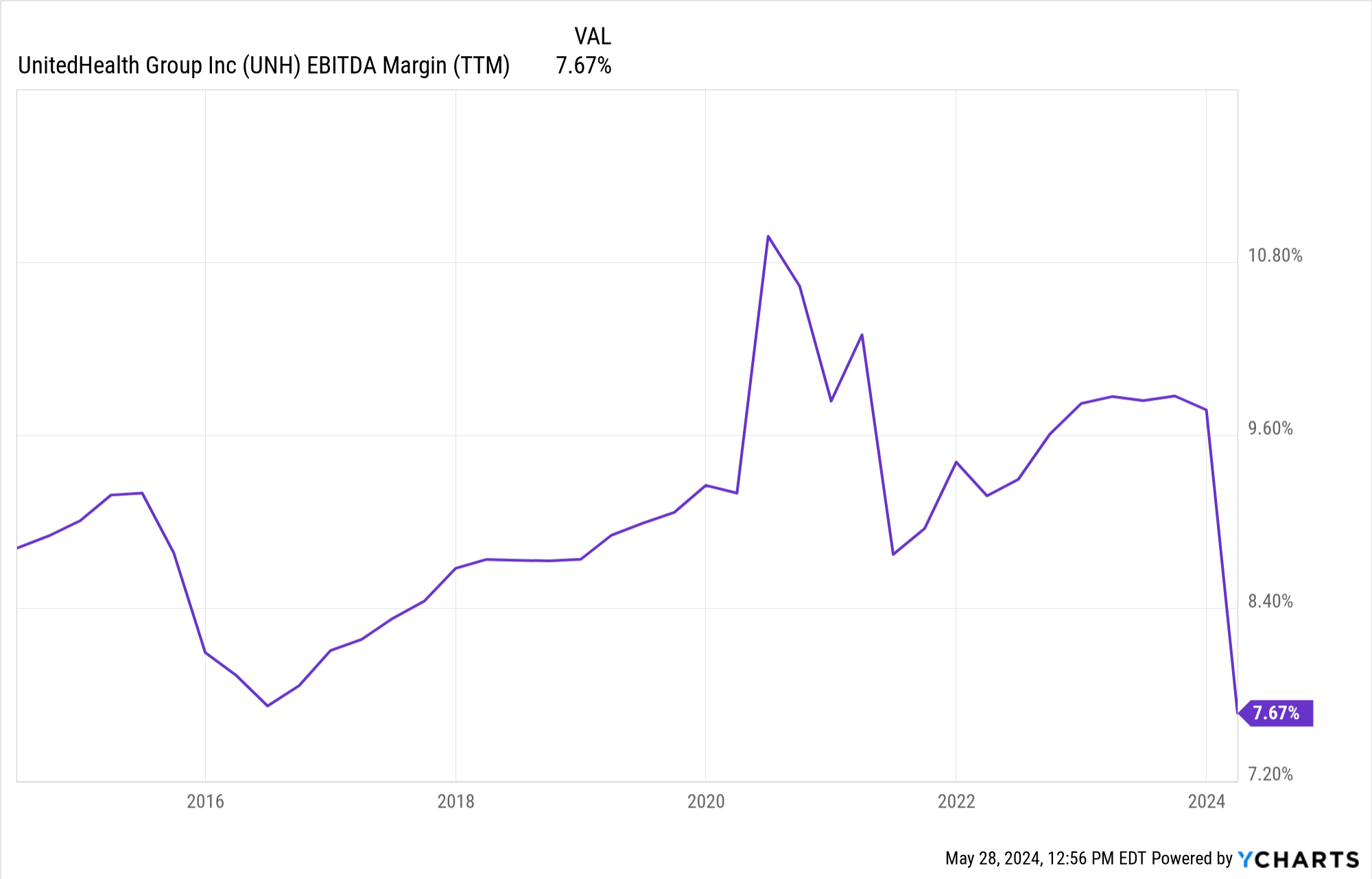

Margin Commentary (Margins are incredibly important to the DCF Model):

We can see below that UNH’s Margins have come under pressure over the past 6-9 months, and this has resulted in the Stock Price being capped at Resistance from a technical structure perspective.

In my opinion, there is no other fundamental variable that drives Stock Prices (in any sector) more than EBITDA growth and EBITDA margin expansion.

This means that any government policies that are going to lift pricing for managed healthcare services will be a boost to UNH’s business model.

As of this post, we know that rate increases have underwhelmed investor expectations. Hence, UNH has been treading water from an investment standpoint in 2024.

Traders, by virtue of participating in a shorter timeframe, will not care as much about the macro story and will be much more focused on finding swing lows/bullish sequences- which we’ll touch upon below.

Valuation

We can see below in the valuation relative to history chart that even though UNH’s stock has been range bound in 2024, its valuation has actually expanded as the Street pins hopes on a recovery in the managed healthcare space.

UNH has seen valuation multiple expansion primarily from EBITDA margins falling from previous Analyst estimates.

This suggests to me that institutional investors are willing to keep providing UNH a valuation premium as its market leadership positioning in managed healthcare could potentially allow it to be one of the first Dow Stocks to perform once sector rotation returns.

DCF Model Outcomes/Scenario Analysis:

The most important inputs in my opinion are 1.) Top Line Growth (Sales) 2.) EBITDA Margins (profitability) and 3.) Valuation Multiple EV/EBITDA (what Investors Pay).

In all scenarios below, I will assume Wall Street Revenue estimates are accurate. The inputs that I change are EBITDA Margins and the EV/EBITDA Multiple. Changing revenue estimates do not move the needle by that much.

I will use more conservative inputs for EBITDA margins and the EV/EBITDA multiple.