Hi Everyone,

We’re going to do a DCF Conclusion Study on Intel (INTC) as I search the tech sector for possible value. Depending on the day, Intel is periodically a top 10 weighted stock within the SOXX ETF.

INTC DCF Discussion/Context

Investors know by this point that Intel is structural laggard in both the Dow and the tech sector. The company has reported revenue guidance resets in the previous quarter which have disappointed investors hoping for a larger turnaround.

Wall Street is generally wary of the turnaround narrative in Intel’s PC segment and believes that its Data Center business will take time to ramp up. Given other growth opportunities in the market, Investors are mostly sidelined on Intel’s stock.

Let’s dive into the DCF Conclusion Study below and see if our model aligns with the Street’s thinking.

Exhibit 1: DCF Core Figures from 2024

Here are the conclusions that I’m drawing:

We can see that the Street expects a ramp up in revenue growth in the upcoming 2 fiscal years but revenue estimates are not provided by most Sell Side firms, indicating a lack of confidence. Out of conservatism, I’m going to use 0-1% top line growth as an input.

As will be shown below, long term Intel EBITDA margins have been falling and this is reflected in the stock’s descending trajectory.

The company’s forward estimates are not as stable as other semiconductor/tech companies due to their competitive positioning facing headwinds.

Margin Commentary (Margins are incredibly important to the DCF Model):

We can see in the chart below that Intel’s EBITDA margins have deteriorated substantially after 2022/2023 as AMD and Nvidia take up considerable market share in the PC segment away from Intel. There are also headwinds stemming from soft demand in its PC and Data Center business.

Most Sell Side firms believe it will require several quarters (at least) to turn around the gross margin story.

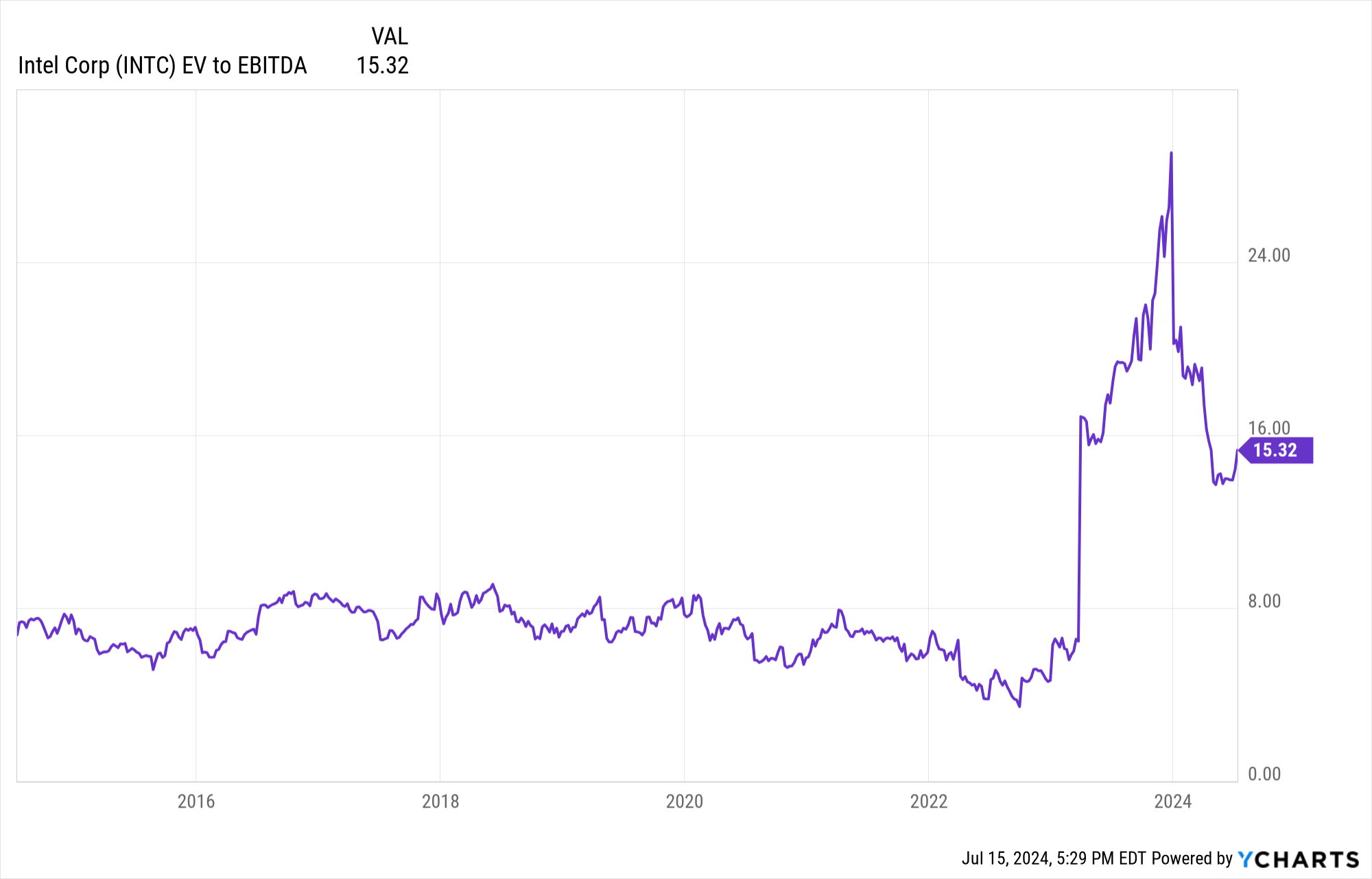

Valuation

Because Intel has seen erosion in its profitability over the past several quarters, its shares’ valuation actually trade more expensively than they did 18 months ago (15.3X today vs. 7-8X in 2021-2022). The company has the opportunity to reset sentiment with new product lines in the coming quarters.

As of now, Investors are in wait-and-see mode.

DCF Model Outcomes/Scenario Analysis:

The most important inputs in my opinion are 1.) Top Line Growth (Sales) 2.) EBITDA Margins (profitability) and 3.) Valuation Multiple EV/EBITDA (what Investors Pay).

In all scenarios below, I will assume Wall Street Revenue estimates are accurate. The inputs that I change are EBITDA Margins and the EV/EBITDA Multiple.

Scenario 1 Assumptions: