4/9 Daily Market Note: DCF Conclusion Study on Lululemon (LULU)

What is the final bearish target on LULU?

Hey Everyone-

This note is going to be one of my DCF Conclusion Studies on a premier company that has recently fallen out of favor with the market: Lululemon (LULU). It’s not just LULU though that has gained bearish sentiment, but also the broader retail sector.

Before we get started on it, feel free to check out my recap on today’s session in a recent Instagram Post shared here.

With that said, let’s get into LULU! Down -30% from its peak and now trading at valuations near COVID, has Wall Street become too pessimistic? And will this one be just like the other retail names (Disney, Dollar General, Dollar Tree) that go through a 4-6 month soft patch only to rally significantly from its local lows.

Let’s discuss below.

LULU DCF Discussion

LULU is one of my favorite names within retail because they have attracted an affluent group of women to buy their premium products - particularly their flagship yoga pants.

From a logical standpoint, yes, there are substitutes to LULU’s products and that means their margins (one of most important levers in Wall Street DCF Models) could come under pressure if other brands gain market share.

On the other hand though, my understanding of the retail market is that IF women can afford to purchase yoga pants/athleisure products at LULU, I believe they don’t really see any other brands that are real substitutes in terms of prestige and image.

In the short-term, LULU may see further weakness. But long-term (this one could take a while), I see LULU at a minimum re-capturing 400+.

It’s one of those names where if you like their story/product, you hold it for a while and be pleasantly surprised in after about 4-5 quarters.

Just like DIS/DG/DLTR in 2023, which took a long time to get its momentum back from local lows, this stock will require considerable patience.

Exhibit 1: DCF Core Figures from 2024

Here are the conclusions that I’m drawing

Wall Street Consensus Revenue Growth Rate estimates after this latest fiscal year have been severely downgraded from the 19%-20% level back to the low 10% region.

EBITDA estimates in 2028-2029 are about 50% higher than they are today, suggesting a materially larger base of operating income (EBITDA) for LULU within 3-4 years.

EBITDA margin forecasts are stable at 26-27% for the upcoming years compared to the latest Fiscal Year, indicating that the Street is not expecting margins to increase (a good conservative call)

Margin Commentary (Margins are incredibly important to the DCF Model):

The Street believes that Lululemon’s EBITDA margins are likely to remain stable without much expansion into the coming years as seen in the DCF Core Figures table above.

I did a 10-year statistical study of LULU’s margin history and it appears today’s margins at 26.9% is rather close to its 10-year corporate high of 27.3%.

In order for LULU to grow margins from here, they would need to release new high-margin products in addition to their core Yoga Pants flagship product and find material success in those categories.

Yes, they have diversified into new products, but I would have wanted to see higher review ratings for their new items. Also, my opinion is that diversification is not always a good thing when it comes to product focus.

My view is that IF the company comes out with a more public statement in future earnings transcripts that they are instead focusing more on their flagship products (women’s yoga pants) to secure complete market leadership, I believe that would interpreted as bullish.

Focus on one big winning product can be a very streamlined way for companies to get their momentum back quickly.

Based on their diversification of products but limitations on raising prices further, I agree with the Street’s projection that margins are likely to remain stable from here and if there is upside, it’s within the realm of a few basis points.

Of course, I would love to be wrong on this aspect because additional margin expansion beyond what is currently expected would open up far further upside than the scenarios shared below.

Valuation

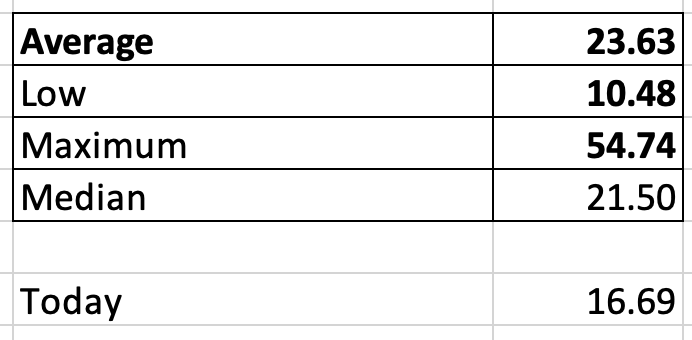

Using EV/EBITDA as a valuation proxy, we can see that investors have de-rated LULU’s valuation potentially for the reasons I discussed above - perhaps, a bit too much diversification into other products can lower the prestige on its core product (yoga pants) which propelled them to stardom.

Still, even with perceived execution issues, LULU still grows 10%+ top line and has a 27% EBITDA margin. This combination makes 16.6X EV/EBITDA not a demanding valuation in my opinion.

We can see in the table above that LULU trades about -30% less expensive than its 10-year historical average and about -20% less expensive than its median valuation.

Is it possible that LULU returns to a 10-11X EV/EBITDA area? Anything is possible, but for now, unless margins decrease (LULU loses pricing power), I view that as a less likely scenario.

DCF Model Outcomes/Scenario Analysis:

The most important inputs in my opinion are 1.) Top Line Growth (Sales) 2.) EBITDA Margins (profitability) and 3.) Valuation Multiple EV/EBITDA (what Investors Pay).

In all scenarios below, I will assume Wall Street Revenue estimates are accurate. The inputs that I change are EBITDA Margins and the EV/EBITDA Multiple. Changing revenue estimates do not move the needle by that much.

Scenario 1 Assumptions:

Wall Street Revenue Estimates for 2027-2028 are accurate

Terminal Year EBITDA margins are 27% (Currently the Street’s Terminal Estimate and the margins as of latest quarter)

Apply a 16.7X EV/EBITDA multiple (Current Valuation)

405-408/share

Note: Within 18 months, I view this as highly probable.

Scenario 2 Assumptions:

Wall Street Revenue Estimates are accurate

Terminal year EBITDA Margins are 24% (10-year historical average)

Apply same 16.7X EV/EBITDA multiple (Current Valuation)

365-370/share

Scenario 3 Assumptions

Wall Street Revenue Estimates are accurate

Terminal Year EBITDA Margins are 20% (10-year corporate low for margins)

Apply 16.7X EV/EBITDA multiple (Current Valuation)

315-320/share

Commentary:

LULU’s current share price of 350-355 implies to me that the Street is losing confidence that the company can hold up its margins and that it could drift to the low 20% region seen in Scenario 3.

However, a 20% EBITDA margin is a 10-year corporate low for the company, and if seen, I think management will do their best to defend that line-in-sand level for profitability via restructuring and/or other corporate strategies.

While I do not enjoy averaging down on a position, I will give this premier brand an exception and be using a second (and last) bullet on LULU if it gets to 310-320 (orange box below) as Scenario 3 showcases a scenario that is too pessimistic in my opinion.

Within 18-months, I think Scenario 1 is highly probable.

Conclusion: My first play into LULU on earnings day (discussed on Twitter) to target 405-410 when it traded 395 was spot-on. However, a light re-entry in LULU in the 385-390 area trapped my direct position and follow-up long call at 360 has been caught up in strong bearish winds. If it is clear to me that the Jan 2025 360 Call will not work within 30-45 days, I’ll convert it into a direct shares position to axe out theta time decay.

I remain confident that Scenario 1 will be achieved in 18 months but that means the path to get there will be longer and will not be easily achieved.

My final entry will be in the orange box 310-320 if it gets there. After that, I will let time do its thing.

I don’t see a need to put a stop-loss on a long-term position. LULU is currently about 3% of my long-term book. If the final entry is placed at 310-320, it will be about 5-6% exposure. I will cap my exposure at 5-6%.

My Personal Playbook on LULU for Community:

The Prudent Move: Wait for 310-320 for a final and last entry.

Risk-Averse: Close the 360 Call at a modest gain if we see 370-380 again on a relief bounce.

-Larry

Link to DCF Archive

https://larrycheung.substack.com/t/dcf-modeling-fundamental-analysis

Note: These are my opinions based on my own research and my model may or may not aligned to the market’s thinking. I have to repeat this in all my notes as there is an element of the unknown in today’s strange macro environment.

Disclaimer: My investment community is not investment, financial, or trading advice, but for educational informational purposes only. I am happy to share my personal opinions which I provide as my personal journal. Trading of any kind of securities involves a lot of risk. No guarantee of any profit whatsoever is made. Investors may lose everything they have. Practice extreme caution. No profit is guaranteed whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this publication are NOT registered as securities broker-dealers or investment advisors either with the U.S. SEC, CFTC or with any other securities/regulatory authority. Make sure to consult with a registered investment advisor, broker-dealer, and/or financial advisor.