11/21 Daily Market Note: Top 6 Charts from latest Bank of America Global Fund Manager Survey - All Hail the Soft Landing

Made Public: 11/21 Premium Strategy Note

Note: This Daily Note is shared with the public. Please share with your network so that we can reach/help more folks. Thank you to Interactive Brokers (pays 4.8% Interest, has European and HK Trading, and offers good execution) for partnering with my content.

Folks-

In this note, while markets run in the background, we’ll go over the recent Bank of America Global Fund Manager survey and observations that I think are notable. I’ll share the charts that represent the overarching big picture macro views.

The core playbook among many institutional investors is that there will be a soft landing in 2024, lower rates, a weaker US Dollar, weaker China macro and continuation of Large Cap Tech strength.

As of this note, 76% of managers believe that the Fed Hiking Cycle is over and 80% expect lower short term rates (see images below). There is now increased positioning towards bonds, REITs (Real Estate), and Japanese stocks. Crowded trades continue to be Long Big Tech, Short China, and Long T-Bills.

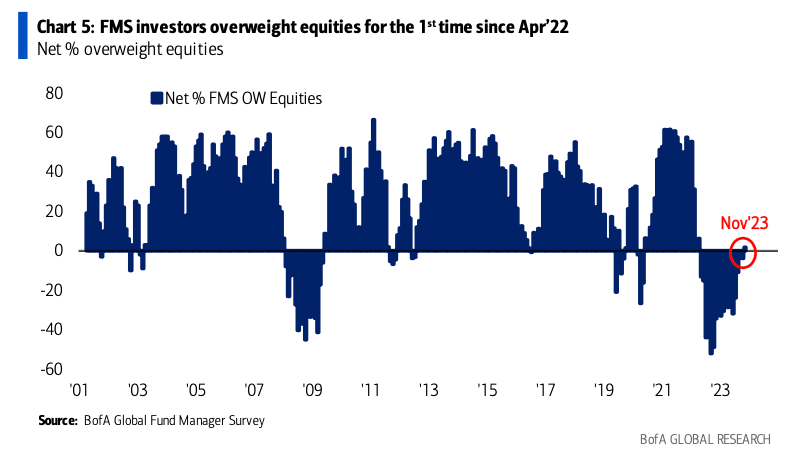

Fund managers are aggressively deploying cash into the market as the average cash balance drops from 5.3% to 4.7% month over month. In this context, investors are also the most overweight bonds since the Global Financial Crisis in 2008. And Investors are, for the first time, overweight equities since April 2022. Month over month, we saw a net 4% underweight turn into to net 2% overweight in stocks.

Investors are positioning for a less bearish profit outlook – reversing pessimism back to levels from February 2022.

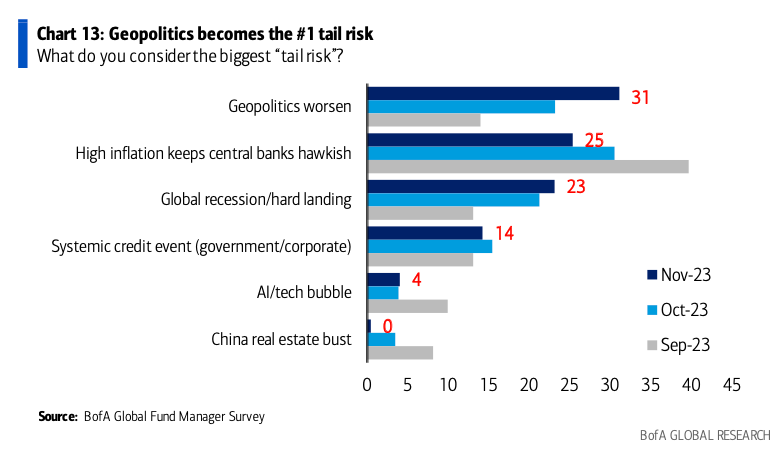

And most believe that the biggest tail risk now is Geopolitics.

To position for this environment, Investors see Bonds as the best performing asset class in 2024.

And in search of alpha, they are also ramping up their bets on Short China Stocks.

My Thinking about this Fund Manager Survey:

Many of these views make sense at the immediate present being validated by recent market pricing but some of them I think may end up being incongruent as time goes on.

Let’s say you are looking for a soft landing, which is now the consensus. In such a case, it should then be Equities that is the best performing asset class in 2024. A soft landing would benefit growth stocks the most and favor a continuation of the current equity market advance. Not bonds. There is no reason for yields to decline dramatically if the economy is still very strong, given that Federal debt issuance is now quite aggressive - to say the least.

Also, declining yields is not always a good sign for a soft landing - it indicates that something more worrisome is about to materialize in the outlook.

A hard landing, which is now an unpopular view, would be the scenario that propels Bonds (TLT) higher and yields lower. Not a soft landing. A soft landing would range-bound Bonds, in my view not cause a new bull market in them. We need a significant rush to safety for Bonds to take off, and that can only be caused by investor distress from the hard landing scenario.

I also do not believe that Shorting China stocks makes a good trade as certain areas of the Chinese economy are beginning to heal (though very slowly). With a lengthened time horizon, there is more upside than downside in the Chinese economy given that we are working off a low base and property struggles are already a widely known fact. Given today’s low valuations in China, shorting a sector that has the potential to recover in EPS estimates over the coming quarters is likely to be a dangerous trade.

Bonds will perform because there is Deflation. Not because there is a soft landing.

Deflation will be a gruesome environment in 2024 for most stocks and sectors.

The concept of Deflation and a Soft Landing is not congruent and don’t go together. You either have one, or another - not both.

I think Deflation is more likely than Soft Landing.

We should be preparing carefully for next steps. We should be building new skills to navigate the market. New ways to properly find companies and sectors that will be positioned well - at the right valuation.

A soft landing after the greatest monetary policy tightening that we’ve seen spanning decades would be unprecedented. Statistics aren’t bullish on a soft landing, and I go by statistics.

But that’s a 2024 story.

Santa is coming in December. And we don’t bet against Santa. 🎅

-Larry

Forward-looking Conclusions of this note:

Macro: Short Sellers are being forced to continue covering their positions leading to higher equity prices.

Stock-Specific: Similar to yesterday, Many stocks are moving towards the Soft Landing scenario – I still like Energy via XOM, and diversified defense such as KR and JNJ

Bonds: 2024 be a year of deflation, any rise in yields will be temporary and an intermittent selloff in TLT back to 84-85 will be buyable.

China: Reiterate positive rating on TCOM for long-term growth.

Positioning: Even if December is seasonally strong, I most likely will be very cash heavy given I’ve accomplished my annual targets – unless there’s anything truly compelling. Leaning ultra conservative and actively researching ideas to go for another 10-20% year in 2024. Not really interested in chasing into year-end.

Please make sure to read my 4-6 previous letters to understand my fundamental/technical/macro views. Every update builds on top of the others. I write quite frequently now so make sure to read many of my previous editions, which often also include valuable educational content to help you grow as an investor/trader. While I do enjoy sharing my personal journaling of the markets, this is not individual customized financial advice.

Tell friends and family about the work we do - I appreciate you. Spread my methodology where I simultaneously employ Fundamentals, Macro, and Technical analysis into my views to help the good folks find alpha.

Disclaimer: My investment community is not investment, financial, or trading advice, but for educational informational purposes only. I am happy to share my personal opinions which I provide as my personal journal. Trading of any kind of securities involves a lot of risk. No guarantee of any profit whatsoever is made. Investors may lose everything they have. Practice extreme caution. No profit is guaranteed whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this publication are NOT registered as securities broker-dealers or investment advisors either with the U.S. SEC, CFTC or with any other securities/regulatory authority. Make sure to consult with a registered investment advisor, broker-dealer, and/or financial advisor.